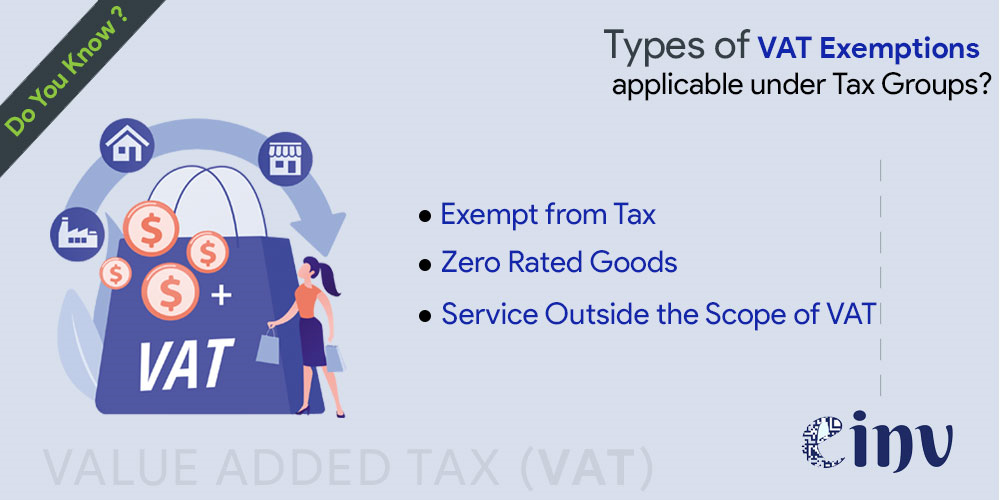

Types of VAT Exemptions

The categories of Value Added Tax (VAT) exemptions applicable within tax groups are outlined as follows:

1. Zero Rated Goods : These are goods for which the VAT rate is 0%. This means you don't pay any VAT on them, but you still need to report them on your tax return. Examples might include exports, certain educational materials, and basic food items.

2. Exempt from Tax : These are goods and services that are not subject to VAT at all. You don't pay any VAT and don't need to report them on your tax return. Examples might include healthcare services, financial services, and religious activities.

3. Service Outside Scope of Tax : These are services that are not considered taxable under the VAT regulations. This means they fall outside the VAT system altogether. Examples might include educational services provided by non-profit organizations, certain childcare services, and postal services.

Differences between Zero-rated, Exempt and Out of scope supplies.

There is a line of difference between zero-rated supplies, exempt supplies and out of scope supplies. Let us discuss in detail:

|

Basis

|

Zero Rated Supplies

|

Exempt Supplies

|

Out Of Scope Supplies

|

|

Meaning

|

Supplies covered under VAT but taxable at 0%

|

Supplies covered under VAT law but have been specifically exempted from tax

|

Supplies that are not covered under VAT law

|

|

Taxability

|

These are taxable supplies, but the rate is 0%. In future, the rate may be changed.

|

These are exempt, i.e. no VAT is leviable. However, they may be made taxable by future notifications.

|

These are out of the purview of VAT and may be covered under other laws.

|

|

Input credit

|

Input is available by way of a refund.

|

Input is not available, and consumers have to bear the burden of VAT on input supplies

|

There is no concept of input credit as such supplies are out of scope

|

|

Example

|

Export of goods and services, international transportation, investment metals

|

Notified Financial services and qualifying residential estate

|

Supplies by persons not registered under VAT supplies not in the course of furtherance of business

|

VATEX Reason Codes & Reason Types Master

Below is the VATEX Master table for your reference:

|

Code

|

Description

|

Code

|

Text

|

|

E

|

Exempt from Tax

|

VATEX-SA-29

|

Financial services mentioned in Article 29 of the VAT Regulations

|

|

E

|

Exempt from Tax

|

VATEX-SA-29-7

|

Life insurance services mentioned in Article 29 of the VAT Regulations

|

|

E

|

Exempt from Tax

|

VATEX-SA-30

|

Real estate transactions mentioned in Article 30 of the VAT Regulations

|

|

S

|

Standard Rate

|

0

|

0

|

|

Z

|

Zero Rated Goods

|

VATEX-SA-32

|

Export of goods

|

|

Z

|

Zero Rated Goods

|

VATEX-SA-33

|

Export of services

|

|

Z

|

Zero Rated Goods

|

VATEX-SA-34-1

|

The international transport of Goods

|

|

Z

|

Zero Rated Goods

|

VATEX-SA-34-2

|

International transport of passengers

|

|

Z

|

Zero Rated Goods

|

VATEX-SA-34-3

|

services directly connected and incidental to a Supply of international passenger transport

|

|

Z

|

Zero Rated Goods

|

VATEX-SA-34-4

|

Supply of a qualifying means of transport

|

|

Z

|

Zero Rated Goods

|

VATEX-SA-34-5

|

Any services relating to Goods or passenger transportation, as defined in article twenty-five of these Regulations

|

|

Z

|

Zero Rated Goods

|

VATEX-SA-35

|

Medicines and medical equipment

|

|

Z

|

Zero Rated Goods

|

VATEX-SA-36

|

Qualifying metals

|

|

Z

|

Zero Rated Goods

|

VATEX-SA-EDU

|

Private education to citizen

|

|

Z

|

Zero Rated Goods

|

VATEX-SA-HEA

|

Private healthcare to citizen

|

|

Z

|

Zero Rated Goods

|

VATEX-SA-MLTRY

|

Supply of qualified military goods

|

|

O

|

Services outside scope of tax / Not subject to VAT

|

VATEX-SA-OOS

|

Reason is free text, to be provided by the taxpayer on a case-to-case basis.

|

NOTE : Incase tax exemption reason code is equal to VATEX-SA-EDU or VATEX-SA-HEA, then the buyer ID is mandatory and must be National ID (NAT)

Author

Jaykumar Vasava

👋 Hello there! , your guide to all e-invoicing things As a passionate, enthusiast and seasoned writer, I'm here to share my insights, experiences, and expertise with you.